Chart of the week

Portfolio Life Vests

Like boaters are urged to add life vests to their water craft, investors are urged to diversify their portfolios as a measure of protection. Stock market downside risk is the biggest risk that most investors face because stocks are generally the most volatile and largest allocation in most portfolios.

The garden variety recommendation investors receive to diversify this risk is to invest in an amount of bonds sufficient to reduce drawdowns caused by stocks to a palatable level. Antti Ilmanen’s great book, Investing Amid Low Expected Returns, also provides data from other protective strategies like trend following, index put buying, long/short quality-minus-junk (QMJ), and real assets like gold.

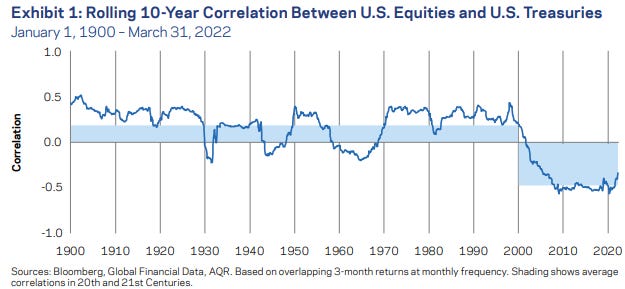

My biggest takeaway when looking at this chart covering 18 of the deepest stock market drawdowns is that bonds have historically not been a reliable life vest when stocks were sinking. Recency bias from the persistent negative correlation between stocks and treasuries during the last 20 years have led many to believe that it will continue, but history tells us that this negatively correlated relationship is tenuous (see below). This negative correlation has powered the conventional 60/40 portfolio to tremendous results recently, but what if bonds don’t continue to serve as the potent diversifier that they have in the recent past? Investors would be wise to diversify their diversifiers and move past only holding bonds to protect their stocks.

Notably, this chart doesn’t include data from this year, one of the worst coincident drawdowns for stocks, bonds, and for the 60/40 portfolio in history.

Data & Chart Source: AQR, Anti Ilmanen - Investing Amid Low Expected Returns