Women lie, men lie, numbers don’t lie1. The inconvenient truth above demonstrates William Sharpe’s observations in his 1991 article The Arithmetic of Active Management. Sharpe begins by saying:

"Today's fad is index funds that track the Standard and Poor's 500. True, the average soundly beat most stock funds over the past decade. But is this an eternal truth or a transitory one?"

"In small stocks, especially, you're probably better off with an active manager than buying the market."

"The case for passive management rests only on complex and unrealistic theories of equilibrium in capital markets."

"Any graduate of the ___ Business School should be able to beat an index fund over the course of a market cycle."

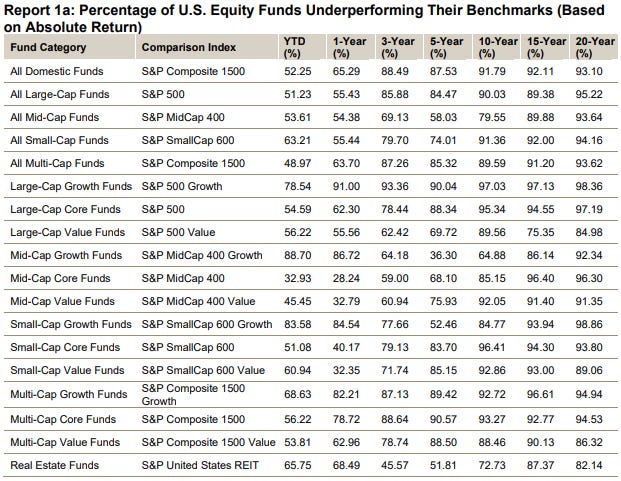

Statements such as these are made with alarming frequency by investment professionals. In some cases, subtle and sophisticated reasoning may be involved. More often (alas), the conclusions can only be justified by assuming that the laws of arithmetic have been suspended for the convenience of those who choose to pursue careers as active managers.

The return on the average actively managed dollar will equal the return on the average passively managed dollar before fees. After fees, the return on the average actively managed dollar will be less than the return on the average passively managed dollar. This impact is compounded over multi-year periods and leads to the carnage in the chart2.

But there will always be those in pursuit of becoming the manager in the ~10% of all managers that outperforms the index over long periods after their fees. For those looking to invest with those few managers it’s challenging to discern which have been lucky in their short term track records and which have elite talent and a process that will persist over time. Michael Mauboussin has written extensively3 on skill versus luck in investing and has great insights in the video below.